.png)

.png)

.png)

.jpg)

%20F%20(1).jpeg)

.webp)

The Listing Act introduced the most significant changes to the Market Abuse Regulation (MAR) since 2016: new disclosure rules for protracted processes, higher sanctions but also tighter expectations from regulators. While the core objective of MAR remains unchanged, to protect market integrity and ensure equal access to information, the way issuers meet these obligations is evolving.

During our webinar “Preparing for the MAR 2026 Changes: What Issuers Need to Know” Tatyana Valkova, Chief Risk and Compliance Officer at Euronext, Petra Heindl, Attorney-at-Law at Kinstellar and Emil Burman, Senior Product Manager for the Compliance Solutions at Euronext Corporate Solutions answered core questions around MAR requirements brought to issuers with the introduction of the Listing Act. The three experts provided different perspectives from legal to practical takeaways and best practices for compliance professionals at listed companies.

Read a short recap of the webinar with the key takeaways.

Are you looking for a clear overview of how the Listing Act changes apply to MAR?

Are you looking for a clear overview of how the Listing Act changes apply to MAR?Download our whitepaper for compliance and legal professionals and share it with your team.

Download whitepaperThe Listing Act brought a change to disclosing inside information in protracted processes. How should an issuer understand the "final event" in a protracted process, including management changes?

Petra Heindl explained that MAR now separates intermediate steps from the final event in a protracted process:

-

Only the final event must be disclosed. Intermediate steps that qualify as inside information do not require disclosure, provided confidentiality is maintained, but they remain subject to insider list, confidentiality and trading prohibition requirements.

-

The European Commission has issued a non-exhaustive list of final events, generally the point at which a process becomes sufficiently definite and concrete to constitute inside information.

-

If confidentiality is lost (e.g., a leak or a sufficiently precise market rumour), disclosure becomes mandatory without delay.

-

Practical consequence: expect longer confidentiality phases, larger and evolving insider groups, active market monitoring, and draft ad hoc notifications kept ready for release.

-

Example of a final event: For a management change, the final event is the decision of the competent governing body (in a two-tier system, the management board) to appoint or remove a board member, disclosed as soon as possible after it is taken. A sudden resignation is a one-off event and not a protracted process. It must be disclosed immediately.

What are the most common struggles or mistakes issuers face under the current MAR regime?

According to the panellists, these are the main pain points:

-

Determining when information becomes inside information. Pinpointing the exact moment at which information meets the MAR definition of inside information remains a key challenge.

-

Identifying and managing inside information at an early stage. Issuers often spend too much time trying to avoid concluding that inside information already exists (for example, through cautious email drafting). A more effective approach is to focus early on confidentiality measures, access controls and maintaining a confidentiality list that can later be converted into a formal insider list

-

Maintaining MAR-compliant records. Issuers often struggle to maintain records in the format expected by ESMA, particularly in relation to retention requirements. MAR compliance should be treated as an ongoing governance responsibility rather than a purely documentary exercise.

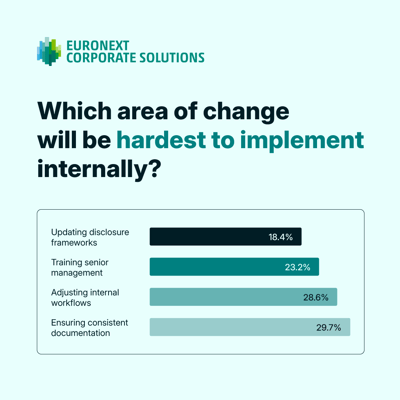

During the webinar, participants responded to the poll question “Which area of change will be hardest to implement internally?”. 28.6% of compliance professionals answered that “Adjusting internal workflows” could be a challenge. Does this reflect what you are seeing in the market?

Petra Heindl confirmed that the reforms affect the whole internal decision-making process – from escalation, identification of decision-maker and involvement of legal and compliance to proper documentation – not just the legal analysis. She highlighted that companies’ internal processes often grow organically without being formalised, which can result in unclear responsibilities and difficulties coordinating across functions and jurisdictions during fast-moving events.

How does Euronext approach regulatory change, using the Listing Act as an example, and what governance practices could other issuers adopt?

Tatyana Valkova recommended that issuers monitor regulatory developments at an early stage and begin preparing before final measures are published. Once the requirements become clearer, issuers should map existing processes against the new rules to identify any gaps and determine where changes may be needed.

Using the Listing Act as an example, she noted that Euronext reviewed the Disclosure Committee's terms of reference, mandate and governance framework and complemented these changes with awareness and training sessions.

As a pan-European market infrastructure, Euronext also monitors how local regulators implement the rules across different jurisdictions to help ensure a consistent approach to compliance. She highlighted the Disclosure Committee as a key governance practice that other issuers could adopt. This involves ensuring the right people are involved at the appropriate level, bringing together diverse functions to support well-informed decisions and maintaining a clear audit trail documenting each decision.

Regulatory change is constant and issuers often know something is coming without a clear view of what it means or where to start. Time pressure pushes teams into a reactive mode. The ones who stay ahead have centralised their compliance processes and tools.

That's what InsiderLog is built for. The all-in-one MAR platform enables you to rely on a single source of truth for insider status, delay of disclosure, trading windows and PDMR transactions.

By centralising your Market Abuse Regulation obligations in a secure platform, you have more control over MAR compliance.

Get more infoWhat does the ESMA aggregated sanctions report show about enforcement focus, and how to be proactive?

Petra Heindl explained that the most frequently sanctioned area remains delayed disclosure of inside information. This typically reflects weaknesses in early identification and in the ability to make timely, justified and well-documented disclosure decisions.

-> Check here a dashboard with MAR sanctions & fines data from ESMA reports

She noted that regulators are also increasingly focusing on deficiencies in insider lists, even in the absence of insider trading allegations with supervisory reviews such as those conducted by the Austrian FMA. In addition, failures relating to PDMR notifications continue to attract sanctions, as they are viewed as indicators of a weak compliance culture.

While the formal sanctions framework under MAR has not materially changed, she emphasised that practical enforcement exposure has increased. Issuers should therefore strengthen governance, improve process management and ensure organisational readiness to demonstrate compliance in practice.

What do issuers tend to underestimate about the operational effort involved in implementing regulatory change?

Emil Burman stressed that it is typically the downstream internal work that is underestimated, including retraining staff, updating templates and reconfiguring workflows by the implementation deadline. He emphasised that organisation-wide education is critical, as the most effective compliance tool is a culture of compliance that extends beyond a single function or team.

What is one key piece of advice for issuers right now?

The panellists emphasised several points:

-

Do not wait to act. Prepare the processes, organisational structures, documentation and supporting tools early to ensure insider lists remain up to date and regulator requests can be answered quickly.

-

Conduct a gap analysis. Assess current arrangements against the revised framework, update templates and delayed-disclosure documentation and review the Disclosure Committee's mandate. Brief the board and senior management, as MAR is increasingly a board-level governance topic.

-

Avoid fragmented manual compliance. Manual MAR processes carry significant risk, particularly under the evolving framework. Centralisation creates structure and structure reduces risk; the key test is whether processes can withstand regulatory scrutiny, not whether they are efficient.

Key Takeaways

-

The Listing Act brings the biggest MAR changes since 2016 — new protracted-process disclosure rules and higher sanctions — entered into force on 5 June 2026.

-

MAR now distinguishes intermediate steps from the final event; only the final event is disclosed, but intermediate steps can still be inside information, so insider lists, confidentiality and trading bans still apply and a leak or precise rumour forces immediate disclosure.

-

Per the ESMA aggregated sanctions report, top enforcement areas are delayed disclosure, insider list deficiencies (even without insider trading) and PDMR notification failures; insider lists are now a core governance tool. Check here how you can fulfill these requirements.

-

The central practical challenge: identifying when information becomes inside information. It is good practice to manage this via a cross-functional Disclosure Committee with a documented audit trail.

-

Shared advice: act early and structure MAR compliance. Run a gap analysis, update documentation and templates, review the Disclosure Committee’s mandate, and brief the board. Move towards centralised processes and tools, as structured governance reduces enforcement risk and improves resilience under scrutiny.